Our relatively low Greenhouse Gas (GHG) emissions are driven by market developments, product evolution and the growing use of less carbon-intensive or even carbon-neutral sources of energy, such as bioenergy, and by investments in energy efficiency.

The sector is becoming increasingly energy self-sufficient by using its own process by-products and residues to generate renewable energy in its Combined Heat and Power (CHP) installations and biomass boilers.

Under the EU ETS, the pulp and paper sector has reduced its fossil carbon emissions by 39% compared to the 2005 levels.

We have achieved a reduction of our total (direct and indirect) carbon emissions by 59% per tonne of product from 1990 to 2024.

Cepi’s Energy Efficiency Solutions Forum (EESF) gathers the European pulp and paper industry, technology suppliers and relevant experts from research, financing and policymaking.

Their remit is to accelerate the development and implementation of emission-reducing technologies, to build awareness on the technological opportunities, to identify obstacles to their deployment and to advocate for a favourable regulatory environment.

Recently, the EESF has collaborated with the heat pump industry and its EU association, and laid the groundwork for heat pumps to be integrated in Europe’s paper mills. Heat pumps have the potential to provide about 50% of the energy required for heat and, in the same process, help to lower their CO2 emissions. g. Creating a favourable regulatory environment. The way forward is to secure an enabling policy framework for the industry to realise its full potential to decarbonise manufacturing processes and further contribute to achieving the European climate neutrality target by 2050.

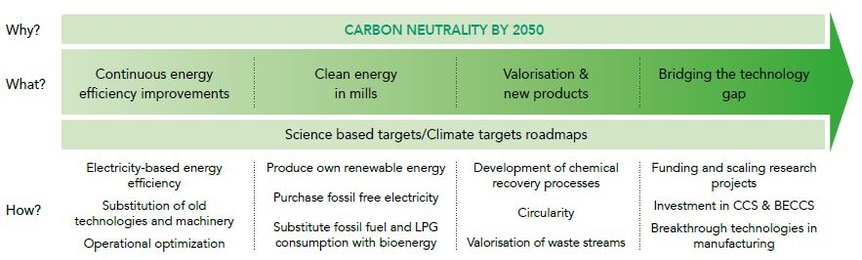

The pulp and paper industry can and will contribute to reaching the 2030 goal and European carbon neutrality in 2050. This requires emission reduction in our production processes by both the implementation of technologies reducing energy consumption and the efficient use of fossil-free energy sources.

How to reach carbon neutrality by 2050?

New business models and financing tools

The huge investments needed in the technological innovations will not be possible without suitable financing tools, new business models and smart cooperation. Cepi’s EESF thus draws attention to the opportunities offered by, for example, EU Innovation Fund, Energy Service Companies (ESCos), Power Purchase Agreements (PPAs, including heat and gas), a voluntary carbon market and Carbon Contracts for Difference (CCfDs).

Breakthrough Technologies

The area with the highest potential for efficiency improvements is the drying process, currently accounting for about 70% of energy used for pulp and papermaking. Three breakthrough technologies have particularly high efficiency potential:

• Superheated steam would enable total recovery of thermal energy, to be used in subsequent processes, resulting in massive energy savings. The challenge is to combine the steam-condensation system with wet paper/water vapour system, requiring advanced steam cleaning technologies and solutions to prevent steam leakage from the system. In Europe, VTT, Valmet, WFBR, RISE and AIT are working together to start a large R&D project in 2023 to pilot a technology towards this by 2026.

• Water removal without evaporation would avoid the most energy-intensive part of the drying process, leading to up to 90% energy saved in drying. In 2022, a consortium of technical universities in the Netherlands started an R&D project to develop non-thermal water removal technologies based on electric forces, aiming for theoretical principles to be translated to industrial equipment by 2024.

Papermaking without water

Papermaking without water offers the potential to remove the use of heat for drying completely. The challenge is to obtain inter-fibre bonding and also dry defibration of pulp or paper for recycling without damaging the fibre. Considerable research is being done on this principle in Germany and Scandinavia. Notably, Swedish PulPac and German BIO-LUTIONS have developed Dry Moulded Fiber, a machine for creating paper products without water. Although ready for market deployment right now, the machine can only create products that make up about 1% of paper demand, leaving much more work to be done to expand to other applications. Further developments towards products with higher market potential are done by the German Modellfabrik Papier, supported by 18 companies and six research centres. Another consortium is EnergyFirst, consisting of 30 paper producing companies from all over Europe and is led by VTT, the Finnish national research institute.

The European Strategic Energy Technology Plan

The European Strategic Energy Technology Plan (SET Plan) aims to accelerate the transition towards a climate neutral energy system through the development of low-carbon technologies. It brings together the European Commission, EU Member States and other interested countries, industry and the research community to coordinate research efforts and investments. The SET Plan identifies ten actions for research and innovation. Action 6 is dedicated to making EU industry less energy, resource and emissions intensive and more competitive. The SET Implementation Plan collates information from industry leaders to support governments in Action 6 areas in the following ways:

– Creating a shared understanding of R&I challenges and opportunities;

– Providing an overview of priority areas to focus R&I efforts for energy intensive industry;

– Identifying priority activities where funding should be targeted (facilitates road-mapping by EC and SET Plan countries);

– Enabling national governments to make informed policy decisions that further support technology development and deployment in these areas

Click here to know more on the Cepi’s Climate Initiative.

Click here to learn more about our vision outlined in our 2050 ‘Investment Roadmap‘ of a low-carbon bioeconomy.

New production technologies ->

Paper production is heat-intensive, mainly due to the large amounts of water to be evaporated in drying pulp and paper. Innovations leading to less water to be evaporated, as well as higher on-site waste heat recovery and co-generation, can increase energy efficiency and reduce emissions. Innovative uses of heat pumps in paper production are being explored to reuse the latent heat from paper drying to produce steam for drying.

The transition to industry 4.0 will also deliver efficiency gains. IEA and Cepi together updated the ETP Clean Energy Technology Guide with Energy efficiency technologies for pulp and paper production.

Low-to no-carbon energy sources ->

The European pulp and paper industry is already the largest industrial prosumer of clean energies, with over 60% renewables in its primary energy consumption. By 2030 the pulp and paper industry has the potential to increase its renewable on-site electricity and heat production to generate almost 31 TWh. This corresponds to 30% of electricity and almost 6% of heat generated on-site in 2020. Read about the full potential here.

Leveraging on-site cogeneration assets ->

Having the possibility to adapt our electricity consumption (demand-side flexibility) offers a range of advantages, such as reduced consumption costs, enhanced generation adequacy and greater accommodation of intermittent renewable energy sources. Provided relevant market and regulatory arrangements are in place, a lot of market potential can be achieved.

Innovative and disruptive solutions ->

The sector bets on breakthroughs in an array of technologies which could reduce the sector’s energy needs by as much as 80%. Superheated steam, waterless papermaking, dry-laying process and non-thermal water removal are some of the innovations identified by the EESF. One of these technologies will eventually become the breakthrough which will allow the sector to significantly reduce its CO2 emissions.

Become a subscriber here